Depreciation: The Backdoor IRA for Real Estate Investors

Every savvy investor knows the power of a tax-deferred retirement account. You contribute money, your taxes go down today, and the government lets you keep that cash working for you — until you eventually pay it back in retirement.

Here’s what most people don’t realize: real estate investors already have one built into every property they own. It’s called depreciation, and it works almost exactly like a backdoor IRA.

How the “Real Estate IRA” Works

The IRS recognizes that buildings wear out over time. To account for this, the tax code lets you deduct a portion of your building’s value each year as an expense — even though you don’t actually spend any money on it.

Critical distinction: land doesn’t depreciate. Land doesn’t wear out, so only the building portion of your property is eligible. That means splitting your purchase price between land and improvements is step one.

A Real Example: 953 King Avenue, Indianapolis

I purchased this property 25 years ago for approximately $32,000, with closing costs of about $2,500. That gives us a total acquisition cost of $34,500.

Step 1: Split Land vs. Building

The county tax assessor had the land at $5,000 and improvements at $45,000 — that’s a 90/10 split. Since assessed value rarely equals purchase price, we use the ratio to allocate acquisition cost:

- Total acquisition cost: $34,500 (purchase price + closing costs)

- Land portion (10%): $3,450 — not depreciable

- Building portion (90%): $31,050 — this is our “IRA contribution”

Step 2: Calculate Your Annual Deduction

Residential rental property depreciates over 27.5 years using the straight-line method:

$31,050 ÷ 27.5 = $1,129 per year in depreciation expense

That’s over a thousand dollars every single year that reduces your taxable income — without costing you a dime out of pocket.

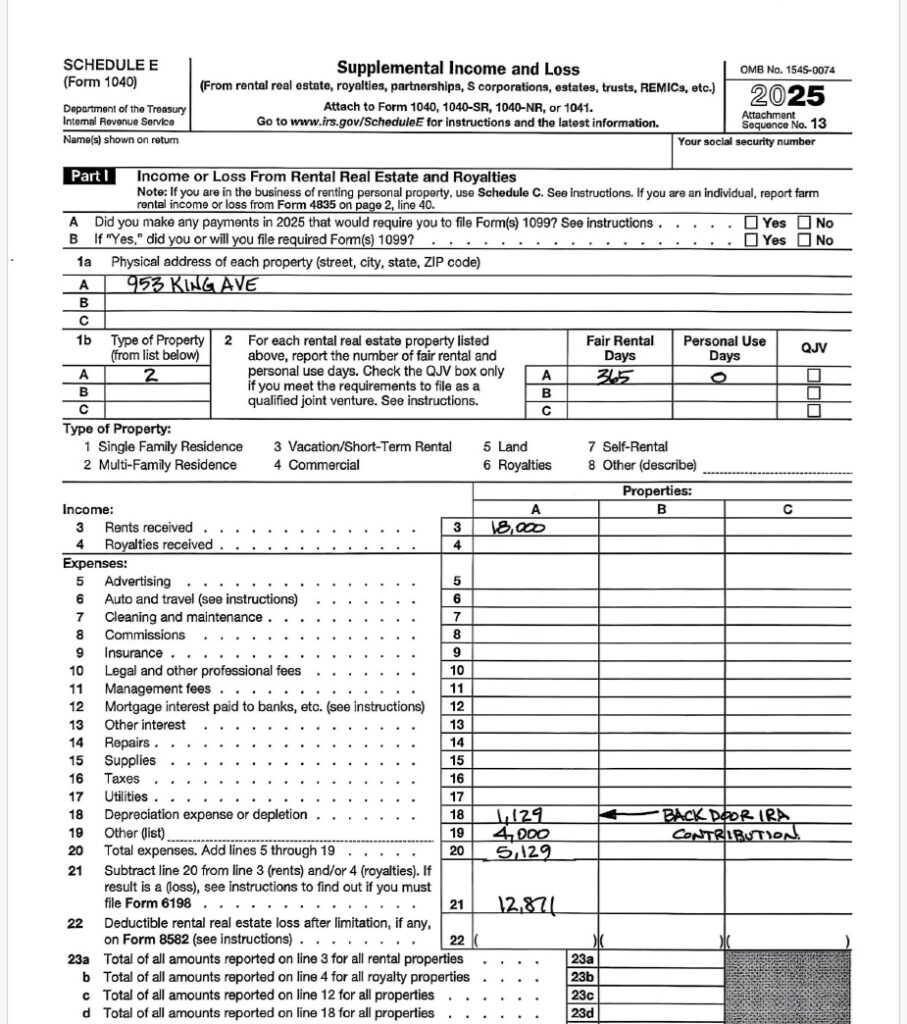

Step 3: See It on Your Tax Return (Schedule E)

On your Schedule E, you’ll see rent income at the top, then real expenses below — taxes, insurance, repairs. And right there among them is depreciation, listed as a non-cash expense that reduces your taxable income.

The Real Impact on Your Bottom Line

This duplex generates approximately $750/month per side ($18,000/year) with real cash expenses around $4,000/year. That gives us:

- Gross rent income: $18,000

- Minus real expenses: $4,000

- Net operating income (before depreciation): $14,000

- Minus depreciation deduction: $1,129

- Taxable income: $12,871

If you’re in the 22% federal tax bracket, that $1,129 deduction saves you $248/year in federal taxes alone. Add Indiana’s state income tax and the total savings climb higher.

The IRA Analogy: Why It Matters

Here’s where the comparison clicks. With a traditional IRA, you contribute money today (reducing your taxable income), then pay taxes on it later when you withdraw. Depreciation works the same way:

- Today: You get a $1,129 deduction that reduces what you owe — just like an IRA contribution

- The difference: Nobody’s writing you a check for depreciation. That money stays in your pocket working for you all year long

- Later: When you sell the property, the IRS “claws back” some of those benefits through depreciation recapture — just like taxing IRA withdrawals

The key insight: you get to keep and invest that deferred tax money for decades. On this $32,000 property, I’ve been parking over a thousand dollars in “deferred taxes” every year. That’s compound growth on money the government let me use instead of taking it.

The Catch: Depreciation Recapture (Your “IRA Withdrawal”)

When you sell the property, the IRS wants to recoup the tax benefits you received from depreciation over the years. The recaptured amount is taxed at a maximum rate of 25% — which is usually still lower than your ordinary income rate.

But here’s the pro move: many investors avoid paying this entirely by doing a 1031 exchange. You sell one property and roll all proceeds into another like-kind investment, deferring both capital gains AND depreciation recapture taxes indefinitely. It’s the real estate equivalent of leaving your IRA untouched — the money keeps working for you tax-free.

The Bottom Line

Depreciation is one of the reasons real estate outperforms stocks on an after-tax basis. Your dividends and capital gains get taxed every year. Real estate lets you defer taxes through depreciation while building equity through mortgage paydown and appreciation — all at the same time.

If you’re evaluating a potential investment property, don’t just look at cash flow before taxes. Factor in depreciation as your built-in tax deferral strategy. You might be surprised how much better the deal looks once you account for that free “IRA contribution” baked into every building you own.

This article is for educational purposes and does not constitute tax advice. Consult your CPA or tax professional for guidance specific to your situation.